A new all-in-one mobile app will offer what its developers claim is Australia’s first end-to-end digital banking platform for the country’s 2.4 million businesses with fewer than 10 employees.

Bankwest is a subsidiary of the Commonwealth Bank, which trades on the Australian Stock Exchange.

Business+ Wades Into Troubled Neobank Waters

The Business+ app is being launched by Great Southern Bank.CEO and Managing Director Paul Lewis said the company had “taken the best of the neo-bank proposition, digitally first, with what we’re good at, which is the banking license side, regulatory requirements.”

Neobanks are digital-only banking platforms that operate solely online. However, in recent years, a string of notable neobanks have struggled to stay afloat including Volt and Xinja.

Now live on Google Play and Apple App stores, Business+ offers everyday transactions, savings accounts, and loans. Within the next few months, Mr. Lewis said, it will also feature secured loans, credit cards, asset finance, and other products for micro-business owners.

“We’ve got the whole package, which I think is a first in Australia,” he said, noting that other neo-banks launched with only a handful of basic products such as savings accounts, but no lending capability.

Small businesses would be able to sign up for an account in under 10 minutes, a time frame he called “fantastic.”

The customer-owned bank also announced on March 8 that it had recorded a 43 percent increase in home loans issued to first-time buyers, and grew its retail deposits by 2.4 percent to $13.33 billion in the six months to Dec. 31.

The transition to a so-called “cashless society” started around 50 years ago with the introduction of credit and later debit cards, but it accelerated during the COVID-19 pandemic, when consumers and retailers were wary of handling potentially infected notes and coins.

Going Cashless Has Its Risks

The disappearance of cash—should it happen—is not without issues, however.In 2022, Tasmania suffered a six-hour internet outage after two of the three cables connecting the state to the mainland were taken offline. All these events affected electronic payment services with lost sale opportunities, and businesses reportedly asking customers to pay with cash.

Associate Professor of Finance at RMIT University Angel Zhong believes that the move to a cashless society in Australia is inevitable, and already well underway.

The trend away from cash also affects marginalised groups.

“We encountered a widespread perception that the elderly are the most reliant on cash, but our research refutes this. For a start, poverty is the biggest indicator of cash dependency, not age,” the report says.

“We identified risks to the viability of rural communities, the loss of personal independence, and increased risks of financial abuse and debt. We don’t believe that leaving this many people behind is an acceptable outcome.”

There is also a risk to “community and connection,” the report says.

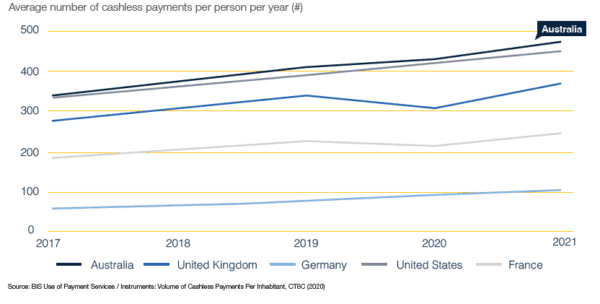

How Fast is Australia Going?

Australia is transitioning to a cashless society faster than almost anywhere else.Cash accounted for only 13 percent of consumer payments in Australia at the end of 2022, in contrast to 70 percent in 2007.

The report concluded that “Australian consumers are fast adopters of cashless and mobile payments ahead of their global peers.”

One of the few faster adopters than Australia is Sweden, where retail payments by cash declined from 40 percent in 2010 to just eight percent in 2022. In the UK, 19 percent of transactions were still made in cash in the same year.

Neighbouring NZ Rejects the Trend

Just across the Tasman Sea, New Zealanders have taken a different approach.A CBDC is issued by a central bank but people do not need a bank account to use it, and it is legal tender, just as with cash.

In an attempt to protect people buying and selling in the digital world, the Australian government has expanded the definitions of “payment system” and “participant” in the Payment Systems (Regulation) Act 1998 to ensure the Reserve Bank of Australia can regulate new and emerging payment systems, such as digital wallet providers and Buy Now Pay Later service providers.

However, the providers mostly oppose any move towards greater control.

Apple, for instance, called the proposal “not a proportionate nor evidence-based regulatory response” and claims, “In the case of Apple Pay, significant investment has been encouraged by regulatory certainty and an absence of unnecessary regulatory intervention.”